Investing in property in Malaysia has long been a popular way to build wealth. With a growing population, urban development, and government incentives, real estate remains an attractive asset.

In 2024, property prices in key areas like Klang Valley, Johor, and Penang continue to show steady growth.

Rental demand is also rising, especially in well-connected areas near public transport and business hubs.

However, buying property isn’t as simple as just picking a house and securing a loan. Investors need to understand market trends, financing options, and potential risks before making a decision.

This guide will walk you through everything you need to know—from choosing the right location to calculating rental yield and managing your investment.

How to Finance Your Property Investment in Malaysia

Understanding Loan Eligibility & Mortgage Pre-Approval

Before buying a property, check if you qualify for a loan.

Banks assess your Debt Service Ratio (DSR) to ensure you can afford the monthly repayments.

Your DSR is calculated as (Total Monthly Debt / Net Monthly Income) × 100. Most banks prefer a DSR below 70%, but this varies based on income and financial history.

Your credit score also plays a crucial role in loan approval. A good credit score increases your chances of getting a lower interest rate. Read more about how to improve your credit score here.

Getting a mortgage pre-approval helps you know how much you can borrow.

Compare home loan interest rates from banks like Maybank, CIMB, and Public Bank to find the best deal.

Here’s an article on the 5 steps to check home loan eligibility from iProperty!

Down Payment & Other Initial Costs

Most banks require a 10% to 20% down payment.

For a RM500,000 property, this means you need at least RM50,000 upfront.

Besides the down payment, factor in stamp duty, legal fees, valuation fees, and agent commissions. These extra costs can add up to 3%-5% of the property price.

Government Schemes & Incentives for First-Time Buyers

If you’re a first-time homebuyer, you may qualify for government schemes like Skim Rumah Pertamaku (SRP), which allows 100% financing with no down payment.

Other incentives include the MyDeposit Scheme, which provides up to RM30,000 in assistance, and the Home Ownership Campaign (HOC), which offers stamp duty exemptions on certain properties.

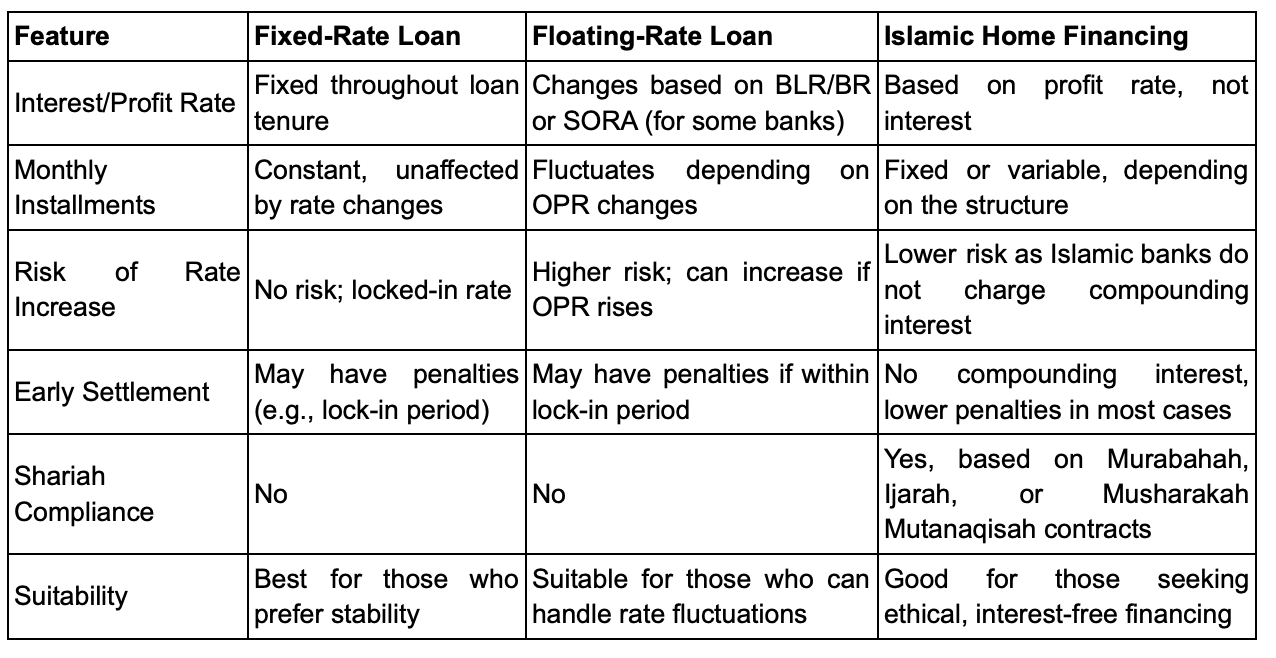

Choosing the Right Loan

Home loans in Malaysia come in fixed-rate, floating-rate, and Islamic financing options.

Which One Should You Choose?

- Fixed-rate loans are ideal if you want predictable monthly payments.

- Floating-rate loans may be better if you expect interest rates to drop.

- Islamic financing is an option if you prefer Shariah-compliant, interest-free home financing.

The loan tenure can go up to 35 years or until age 70, whichever comes first.

A longer tenure reduces monthly repayments but increases total interest paid.

Tips on Financing

Use mortgage calculators on iMoney or RinggitPlus to estimate your monthly repayments.

Make sure your loan fits within your budget and financial goals.

Getting the right financing is key to a successful property investment.

Plan your finances wisely to avoid cash flow problems in the future.

Choosing the Right Investment Property in Malaysia

1. Location, Location, Location

The right location determines your property’s value and rental demand. Look for areas with strong job markets, public transport access, and upcoming infrastructure projects.

Popular hotspots in Malaysia include Klang Valley, Johor Bahru, and Penang, where property prices and rental yields are steadily growing.

2. Property Type: Landed vs. High-Rise

Which One is Right for You?

- Landed property is better for long-term capital appreciation and family living.

- High-rise property is better for rental income and affordability, especially in city areas.

Best Areas for Landed Property Investments 🏡

These areas attract families and long-term homeowners, leading to higher capital appreciation.

- Kajang, Selangor – Affordable landed homes with MRT access and education hubs.

- Semenyih, Selangor – Growing township with affordable new landed developments.

- Setia Alam, Selangor – Well-planned township with good amenities and community living.

- Eco Majestic, Semenyih – A gated community with modern landed properties.

- Mont Kiara, Kuala Lumpur – Luxury landed homes with high-end expatriate demand.

Best Areas for High-Rise Property Investments 🏢

These areas have high rental demand from young professionals, expatriates, and students.

- Mont Kiara, Kuala Lumpur – Popular with expats, high rental yields, and luxury condos.

- Bangsar South, Kuala Lumpur – Near corporate offices, attracting working professionals.

- KLCC & Bukit Bintang, Kuala Lumpur – Prime city area, strong demand for Airbnb and luxury rentals.

- Subang Jaya, Selangor – High student rental demand near Sunway, Taylor’s, and Monash University.

- Penang (Bayan Lepas & Gurney Drive) – High demand from expats working in the tech industry.

3. New vs. Subsale Properties

New properties come with modern designs and lower maintenance but may take time to complete.

Developers often offer rebates, reducing upfront costs.

Subsale properties let you inspect the unit before buying, and rental demand is easier to predict. However, they may require renovation.

4. Developer & Project Reputation

Research the developer’s track record to avoid delays or poor-quality projects. Look for trusted developers like Sunway, EcoWorld, and Sime Darby.

Check online reviews, project completion history, and past buyers’ feedback before making a decision.

5. Match Property to Your Goals

If you want long-term appreciation, choose properties in high-growth areas. For steady rental income, pick locations with strong tenant demand.

Do your research, compare options, and invest in a property that aligns with your financial goals.

Calculating Your Returns: Rental Yield vs. Capital Gains

1. Understanding Rental Yield

Rental yield measures how much income a property generates compared to its price. A higher rental yield means better cash flow.

Use this formula to calculate gross rental yield:

(Annual Rental Income ÷ Property Price) × 100

For example, if you buy a condo for RM500,000 and rent it out for RM2,000 per month, the annual rental income is RM24,000. Your rental yield is:

(RM24,000 ÷ RM500,000) × 100 = 4.8%

2. What is a Good Rental Yield?

A 4%-5% rental yield is generally considered good in Malaysia.

Prime areas with high demand, such as Klang Valley and Johor Bahru, often fall within this range.

However, properties with lower yields can still be worthwhile if they have strong potential for price appreciation.

3. Understanding Capital Gains

Capital gains refer to the profit made when selling a property at a higher price than its purchase cost.

This is where long-term investors build wealth.

For example, if you buy a house for RM500,000 and sell it for RM700,000 five years later, your capital gain is RM200,000.

4. Factoring in Costs

Your net return depends on costs like loan interest, maintenance fees, property tax, and agent commissions.

Always calculate your net rental yield after deducting these expenses.

For capital gains, consider Real Property Gains Tax (RPGT), which applies when selling a property within the first five years.

5. Which Strategy Works Best?

If you want steady passive income, focus on rental yield.

If you prefer long-term wealth growth, aim for capital appreciation.

The best investment balances both strategies—choosing a property with good rental demand and strong future value.

Managing Your Property Investment in Malaysia

1. Finding and Managing Tenants

A good tenant ensures steady rental income with minimal issues.

List your property on platforms like PropertyGuru, iProperty, or Mudah.my to attract potential renters.

Screen tenants carefully by checking their employment status, rental history, and credit score.

A tenancy agreement protects your rights and outlines payment terms.

Here’s a guide on finding good tenants from PropertyGuru!

2. Handling Maintenance and Repairs

Regular maintenance keeps your property in good condition and prevents costly repairs.

Allocate 5%-10% of your rental income for upkeep.

Respond to tenant complaints quickly to maintain good relationships and avoid vacancies.

A well-maintained property attracts long-term renters.

3. Property Management Services

If you don’t have time to manage the property, consider hiring a property management company.

They handle tenant screening, rent collection, and maintenance.

Management fees range from 5%-10% of monthly rental income, but they save you time and effort in the long run.

4. Keeping Track of Finances

Monitor your rental income, mortgage payments, and expenses to ensure profitability.

Use tools like Google Sheets to track cash flow.

Set aside a reserve fund to cover unexpected costs like repairs or vacancy periods. Staying financially prepared prevents stress.

Here’s a list of 21 hidden or unexpected costs of owning a home from Citizens Bank!

5. Staying Updated with Market Trends

Property values and rental demand change over time.

Keep an eye on new developments, government policies, and interest rates that may affect your investment.

Join property forums and follow real estate news to stay informed. Adapting to market trends helps you maximize your returns.

New Strait Times: https://www.nst.com.my/property

EdgeProp: https://www.edgeprop.my/news

PropertyGuru: https://www.propertyguru.com.my/property-news

iProperty: https://www.iproperty.com.my/news

Common Mistakes to Avoid

1. Not Doing Enough Research

Many new investors rush into buying without understanding market trends. Always research location, rental demand, and future developments before making a decision.

Ignoring past price trends can lead to overpaying for a property.

Use platforms like Brickz.my or iProperty.com.my to compare historical transaction prices.

2. Overstretching Your Budget

Buying a property beyond your financial means can cause long-term stress.

Ensure your Debt Service Ratio (DSR) stays below 70% to avoid financial strain.

Unexpected costs like maintenance fees, taxes, and repairs can add up. Always have an emergency fund to cover these expenses.

3. Choosing the Wrong Loan

Some buyers pick a mortgage with high interest rates or inflexible terms.

Compare home loan offers from different banks using iMoney or RinggitPlus.

A longer loan tenure reduces monthly payments but increases total interest paid.

Find a balance that fits your financial goals.

4. Ignoring Rental Yield and Capital Gains

Focusing only on property appreciation without checking rental yield can hurt cash flow.

Aim for a rental yield of at least 4%-5% for a sustainable investment.

If a property has low rental demand, you may struggle to cover loan repayments.

Always check rental listings in the area before buying.

5. Not Having a Clear Exit Strategy

Many investors buy properties without a long-term plan. Decide whether you want to rent, sell, or upgrade based on market conditions.

Selling too soon may trigger Real Property Gains Tax (RPGT), while holding too long in a stagnant market can limit returns.

Plan your exit wisely.

Alternative Ways to Invest in Property in Malaysia

Buying physical property isn’t the only way to invest in real estate.

If you prefer a lower capital requirement and more liquidity, consider these alternative options.

1. Real Estate Investment Trusts (REITs)

REITs allow you to invest in commercial properties, malls, and office buildings without owning them directly. They generate income through rental earnings and distribute dividends to investors.

In Malaysia, you can invest in REITs through Bursa Malaysia, with some offering dividend yields of 5%-7% annually.

Examples include:

- Sunway REIT (5180.KL) – Invests in malls, hotels, and offices.

- IGB REIT (5227.KL) – Owns Mid Valley Megamall and The Gardens Mall.

- Axis REIT (5106.KL) – Focuses on industrial and logistics properties.

Learn more in my guide to REITs.

2. Property-Backed Exchange-Traded Funds (ETFs)

ETFs track property-related indexes and offer diversification with lower fees than direct property ownership. Some ETFs invest in a basket of REITs or property stocks.

Examples of property-related ETFs:

- ABF Malaysia Bond Index Fund (0824EA.KL) – Includes property-related government bonds.

- Global X SuperDividend REIT ETF (SRET) – Provides exposure to global REITs with high dividends.

For a more passive approach to real estate investing, check out my guide to ETFs in Malaysia.

3. Property-Related Stocks

You can also invest in real estate developers and construction companies listed on Bursa Malaysia.

Stocks like Sunway, UEM Sunrise, and EcoWorld offer exposure to Malaysia’s property market.

Examples of property stocks:

- Sunway Berhad (5211.KL) – A diversified developer with real estate, healthcare, and REIT investments.

- UEM Sunrise Berhad (5148.KL) – Focuses on high-end residential and mixed developments.

- Eco World Development Group Berhad (8206.KL) – Specializes in township and sustainable property developments.

Which Option is Right for You?

If you want steady income, REITs are a great option.

If you prefer diversification, ETFs offer a balanced approach.

For those willing to take on more risk, property stocks may provide higher returns.

These alternatives let you invest in real estate without huge capital or the hassle of property management. Consider adding them to your portfolio for a diversified approach to property investment!

Conclusion

Investing in property in Malaysia can be a great way to build wealth, but it requires careful planning.

Choosing the right location, securing good financing, and managing your investment wisely will set you up for success.

Avoid common mistakes like overstretching your budget or neglecting rental yield. A well-researched investment can provide both passive income and long-term capital growth.

Have questions about property investment? Share your thoughts in the comments or follow my blog for more insights on building wealth in Malaysia!